Our CSRD services for you

Does your company fall under the Corporate Sustainability Reporting Directive (CSRD)? This will be the case for large capital market-oriented companies from the 2024 reporting year onwards. Companies that fall under the directive will in future have to provide extensive information on sustainability in their annual reports.

:response supports you in your optimal preparations for the reporting requirements – from CSRD-compliant materiality analysis to the alignment of sustainability strategy, processes, and data management with CSRD requirements, right through to the preparation of the report.

What is the CSRD?

The EU Corporate Sustainability Reporting Directive (CSRD) replaces the previous non-financial reporting requirement (EU Non-Financial Reporting Directive, NFRD). The EU’s goal is to put sustainability reporting on an equal footing with financial reporting.

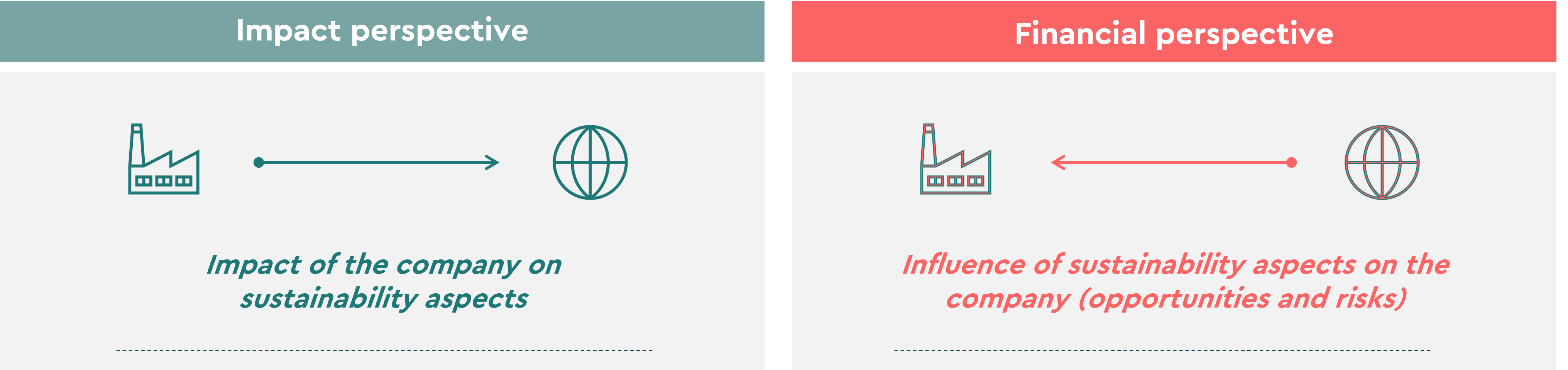

A central part of the CSRD are the European Sustainability Reporting Standards (ESRS), the EU’s uniform standards for sustainability reporting. Companies that are required to comply with the CSRD for sustainability reporting in the future must apply these binding European standards. The standards require disclosures on environmental, social, and governance issues—on the impact on sustainability, on sustainability risks and opportunities for business activities, and on targets, processes, and measures to counteract these. These qualitative disclosures are supplemented by key figures, including those relating to climate, natural resources, and human resources.

Who is affected by the CSRD?

Reporting in accordance with CSRD will become mandatory from the 2024 reporting year for large capital market-oriented* companies and from 2028 for all large companies. Large companies are defined as those that meet two of the following criteria:

(1) more than 1.000 employees

(2) more than 450 million Euro in revenue

Small and medium-sized listed companies will fall within the scope of application in the coming years. With the CSRD, sustainability reporting will become a mandatory part of the annual report and must be published in electronic form (single electronic reporting format). The contents of the sustainability report must also be subject to an external audit with limited assurance.

Due to the extensive requirements of the European Sustainability Reporting Standards, we recommend preparing for the reporting obligation at an early stage. We are happy to assist you in this process.

*All capital market-oriented companies with more than 500 employees and a balance sheet total of more than €25 million or sales of more than €50 million.

Our CSRD services for you:

- Gap analysis: Comparison of existing sustainability strategy, data management, and reporting processes with CSRD/ESRS requirements

- Roadmap for the step-by-step implementation of the requirements from CSRD/ESRS

- Conducting a materiality analysis in accordance with CSRD based on the principle of double materiality

- Analysis of sustainability risks

- Consulting support for the introduction and further development of strategies and processes for sustainability management

- Identification of qualitative disclosures and metrics to be collected in accordance with CSRD, as well as advice on data collection and the establishment of data management systems

- Conceptualization and creation of a sustainability report or chapter of the annual report

Double Materiality Analysis:

Contact us

We are here to answer your questions. Together with our customers, we create an environment in which people enjoy getting involved. We create value for people, organisations and society.